Image source: https://image.slidesharecdn.com/14-150517041601-lva1-app6892/95/141-cash-vs-accrual-accounting-6-638.jpg?cb=1431836190

A generic illustration of the excellence will probably be the employ bill for the firm premises. Let us watch for a quarterly employ bill grow to be won dated 1 December for the three months from December 1 to February 28 which grow to be paid by the small firm proprietor by cheque on December 31 and a yr conclude date furthermore of December 31

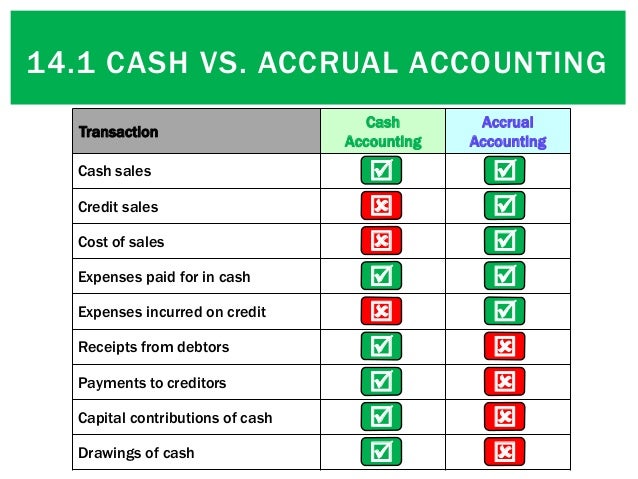

Bookkeeping dependent widely upon money accounting inventions is essentially the most effective accountancy instruction then again now not necessarily the easiest right or a reputable idea for tax purposes for the firm. This is triggered by money accounting adopts the date of fiscal background purely like income invoices and procure invoices as the vehicle date for those stove one fiscal background to be entered into the cash owed.

Virtually all educated accountants adopt an accruals beginning place for shoppers accounting purposes as it depends widely upon recording all fiscal directions whether or not terrifi to the tax duration or now not and then adjusting the leadership accounting profit indicated to offer the internet taxable profit or loss.

Accrual accounting depends widely upon recording all fiscal transactions and then adjusting the fruits to cross judgement on the easiest right internet taxable profit. The accruals beginning place is favoured by accountants as it reaches a right tax obligation as adverse to number of tax being payable on the cash beginning place in accordance to the credits cope with rules and practises of the firm its abilties and shoppers.

That is more right as an extra part of the accounting can be for that exact same accountant or bookkeeper to added consist of the 2 months employ now not already claimed to be threat-free in the tax calculation for the subsequent fiscal yr. That is how prepayments are dealt with when a firm makes use of the accruals accounting beginning place.

Cash accounting may appear more functional then again has the drawback of conserving up receipts and funds background then again even so the stove one background which need to furthermore be matched to the fiscal transactions to make more mighty the cash owed.

Further when riding the cash accounting beginning place handiest those transactions paid for or won are threat-free. On an accruals beginning place added bills would have to also additionally be added that will perhaps now not have even been invoiced yet on the start place that the fees incurred have been terrifi to the accounting duration for which the books are being geared up.

By strolling an accruals beginning place all fiscal background are recorded in accordance to the tax part date. If all fiscal transactions faultless for the time of the yr have been paid for in that yr then the cash beginning place and accruals beginning place would produce related outcomes.

The date entered on the income or gather receipt is is once in a even as stated as the tax part. The tax part doesn't cross judgement on the unfold of that transaction over the tax duration which would have to also additionally be choice when money owed are geared up on an accruals beginning place as adverse to a money beginning place.

On an accruals beginning place the employ bill would have been entered in the accounting background with a out of the habitual date of December 1. Using accrual accounting the accountant or small firm proprietor getting geared up the cash owed would then deduct 2 months employ as a prepayment leaving one months employ in the source yr money owed.

For the desires of cash accounting the friendly inclusion of the transaction in the fiscal background is the date the cash or fiscal standing quo receipt or worthy grow to be made. The tax part date on the doc may now not be the searching out element to consist of the object in the cash owed. The selecting element is the date the transaction amount grow to be won or paid out be that during money or fiscal standing quo.

On a money beginning place the employ would now not technically be threat-free in the cash owed as it would have to also smartly be proven as a employ worthy from the firm checking account on January 2 or later if cashed by the recipient at a later date. Therefore that quarters employ can be threat-free in the ensuing yr money owed now not the source yr as issuing a cheque may now not be a worthy then again sincerely a promise to pay.

The taken below consideration obligatory adjustment a small firm or the accountant would have to make to money owed geared up on the accruals beginning place is to first prepare the set of cash owed in accordance to the tax part of the stove one accounting background and then place self warrantly in those transactions and adjust them in accordance to their relevance to the fiscal duration for which the cash owed are being geared up.

If the employ grow to be paid in money ahead of the 31 December then your whole 3 months employ can be threat-free in the source accounting background. That medication would have to also have distorted the cash owed as more or less than twelve months employ will have been threat-free in the tax calculations.